Merry Christmas and a Happy New Year to all of you! I hope you all had a great holiday season, I know I did. I got to celebrate Christmas with my family and couple days later have second Christmas with my girlfriend's family, and I got some pretty good gifts; my girlfriend's family gets a little crazy with the gift giving.

This is my 4th monthly roundup and I hope to use these posts to discuss my current state of affairs including income/expenses, stock buys and sells, dividend income, and of course my progress on all of my yearly goals. With this being the end of they year and all I was not sure how to handle this post. But I have decided I will first wrap up December (this post), then I will post a separate piece to wrap up the year, and finally I will have a third post that lays out my 2015 budget and goals (or maybe two posts if it gets long).

Income/Expenses:

My expenses are listed to the side. On each line I have the budgeted amount per month, the actual

amount spent for the month of December.

My total expenses were just over $2,000, which is which is actually my best month yet. This is a bit of a surprise with it being gift season but I knew going into this month that I would have to keep my budget tight if I wanted meet my 50% expense rate goal. It also helped that I have been spending more time at home(s) (whether mine, my family's or my girlfriend's) thus leave less opportunities to go out and spend money.

The only category I was over on this month was my "Other" category where all my gift purchases ended up. But I reality this is offset by some birthday and Christmas money I received this month.

INCOME:

Paycheck: $ 6,056.This was a three paycheck month so my income saw a real boost for the moth

% Expenses = 33% of income. A great month (best month ever) but was really boosted by the extra paycheck.

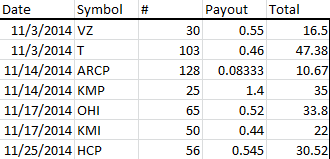

Dividend Income:

Because I have been working hard on paying down my debts, I haven't been able to add much to my portfolio this year. But the great thing about dividend investing is that its still working whether I am adding to it or not. This month I earned $156 without lifting a finger, not bad. The following companies paid me this month:

Buys/Sells:

December was another boring month for trading for me, in the past this is due to me focusing on paying down my student debt but now most of my debt is resolved so I don't have much of an excuse other than a lack of time to perform research.

FRIP

Scottrade offers a Flexible Reinvestment Plan, where dividends from qualifying companies can be used to purchase shares in any other qualifying companies without any commission. So I take advantage of this every month and I usually use it to build up my positions in companies where my positions are lagging.

This month my dividends were used to purchase 6 shares of Kimco Realty Corporation (KIM) .

Net Worth

Net worth will always be a secondary goal for me with generating passive income being my primary goal. But net worth is something I have started tracking. Given how much of my net worth is in stocks, my net worth will have a tendency to fluctuate frequently with the market but hopefully my net worth continue an overall upward trend over time.

Assets:

- 401k: $71,803

- Investments: $63,971

Liabilities

- Student Loan 1: $0

- Student Loan 2: $6,866

- Car Loan: $9,150

NETWORTH: $119,758 down 1.5% from last month

Goals:

- Spend less than 50% of my net income - This was another good month and should keep my on track for meeting this goal.

- Pay off one of my student loans - COMPLETE

- Keep taxable income in the 25% tax bracket - My current federal taxable income is $86,779 from my day job and considering dividends, capital gains, and interest I am about 99% of the way to the 25% bracket limit of $89,350 so this is really close, and I'm not exactly sure about how much my "other" incomes will amount to.

- Weight under 200 lbs - My current weight is 210 lbs which is higher than last month's, Christmas time is not go for weight loss. I don't think I will make my goal but I think I have been putting on muscle lately so I guess its OK. I'll have to revise this goal for next year.

- Run a half marathon - COMPLETE

- Complete the Tough Mudder - COMPLETE

- Work out my legs regularly - I have not been as good as I would like you to be but I have been better than in the past. This one still needs some work.

- Increase my running pace - I have not been running lately because of all of basketball games so I need to figure some way to incorporate running back into my routine, perhaps I will start running on the treadmill at the gym as a warm up before a workout.

- Take an online class - I have chosen a class but have yet to start, when will I find the time? I don't think I will get this goal done this year.

- Work through my backlog of magazines - I finished some of my other books so now I have more time to work through these magazines. My girlfriend would be very happy if I complete this goal, she's tired of the magazines lying around.

Photo Credit: freedigitalphotos.net

.jpg)